Everyday slip-ups, mail quirks, and tiny typos—not neglect—create unclaimed assets

Most unclaimed money doesn’t vanish because someone was careless. It slips out of reach through ordinary, boring problems: an address that never got updated, a name that changed after marriage, a check that looked like junk mail, or a typo in an apartment number. When contact fails and there’s no account activity for long enough, companies must classify the balance as unclaimed and transfer it for safekeeping until an owner (or heir) proves entitlement.

The common paths to “unclaimed”

Moving without updating every account

Forwarding your mail helps, but it’s not a silver bullet. If payroll, insurers, card issuers, brokerages, or utilities never receive the new address, statements bounce, tax forms and checks return, and the clock toward unclaimed status starts.

Small data mistakes with big consequences

A transposed ZIP digit, “Unit 21” entered as “Unit 12,” or a hyphenated surname stored without the hyphen can block delivery and break identity matching. Systems won’t connect the dots; outreach fails.

High-volume clerical misses

At scale, even well-run institutions misapply credits, stale-date checks, or misfile payments. If the owner doesn’t notice—and the institution can’t reach them—the balance ages into reportability.

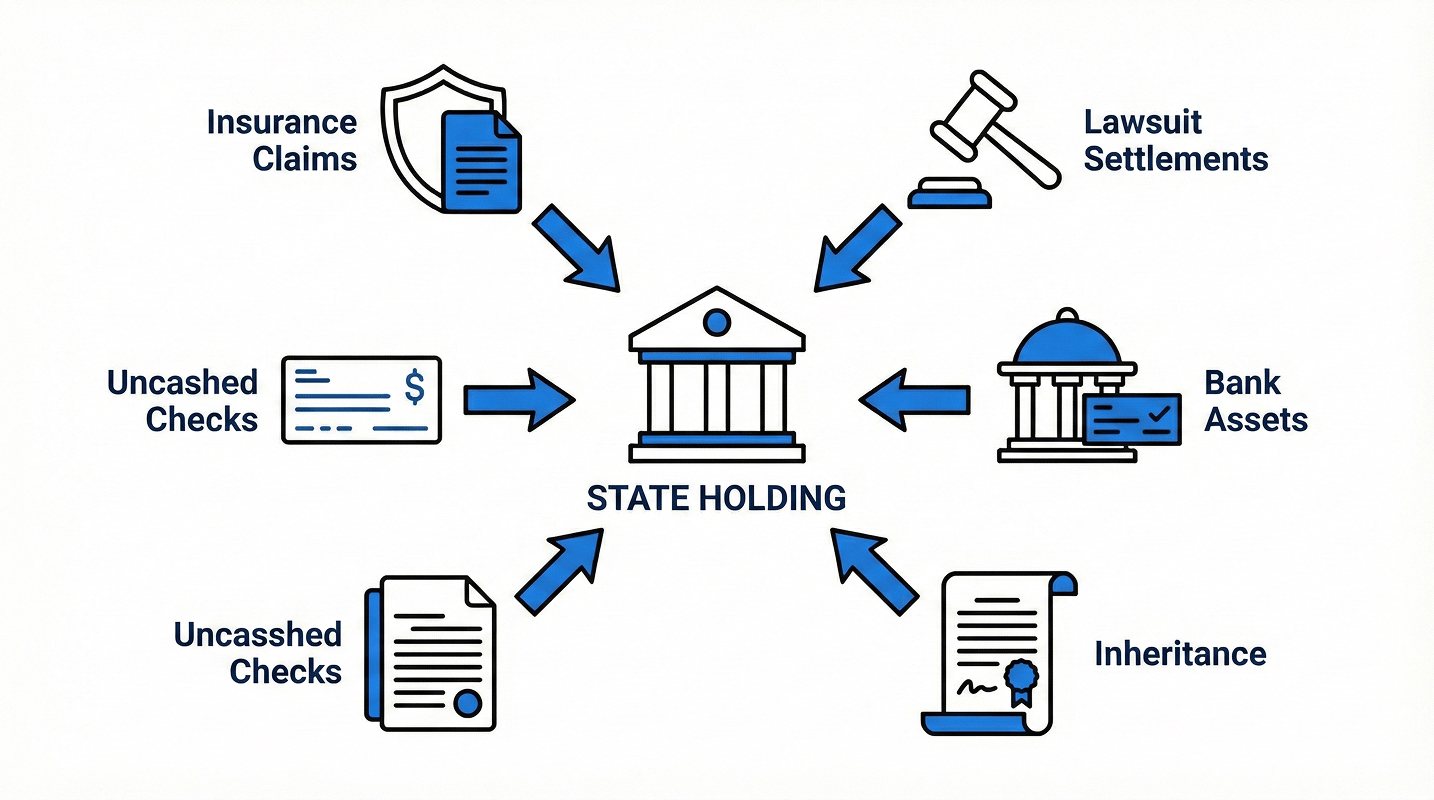

Insurance and employer benefits nobody knew about

Beneficiaries often don’t realize a policy exists, can’t locate documents after a death, or don’t recognize the company name after mergers. Premium refunds, death benefits, and employer plan payouts can sit unnoticed.

Checks that never get cashed

Refunds and dividends sometimes arrive in generic envelopes or during off-cycle periods. If a check expires, the funds are later reported as unclaimed.

Name changes, mergers, and rebrands

Marriages/divorces, corporate acquisitions, or rebranded financial apps create name mismatches. Owners don’t recognize the mailer; institutions don’t recognize the owner.

Paperless pitfalls

Going paperless is convenient—until an alert lands in a spam folder or the email on file is obsolete. Silent credits can go dark without a physical reminder.

The rules in plain terms

- Dormancy period: After a defined stretch with no owner contact or account activity (commonly 3–5 years, varying by asset type and state), a balance is presumed abandoned.

- Due diligence: Before reporting, the holder must attempt contact—typically a mailed notice to the last known address and, if available, electronic outreach.

- Report & transfer: If contact fails, the asset is reported to the state and transferred for safekeeping under unclaimed-property law.

- Owner rights: The money isn’t confiscated; it’s held for the owner or heirs and can be claimed with proper proof. In most cases, there’s no expiry on the right to claim.

Securities may involve additional steps (e.g., liquidation or safeguarding), and certain benefit types have their own statutory triggers.

Why this keeps happening—even to careful people

- Data has to be perfect for automated systems to find you; one typo can sever the only path back.

- People juggle more accounts than ever—employers, banks, brokerages, fintech apps—which increases the odds a small balance gets missed.

- Life events scramble records (moves, marriages, divorces, estates, guardianships).

- Corporate changes hide signals (mergers, servicer changes, or renamed products).

- Digital + autopay = out of sight—few statements, fewer reminders, less friction to notice a stray credit.

Typical dormancy windows (illustrative)

- Bank/credit-union deposits: ~3–5 years without activity

- Wages/Payroll: ~1–3 years after payable date

- Insurance proceeds: ~3–7 years after due and payable

- Brokerage/Securities: activity/contact-based, varies by state and property code

- Safe-deposit boxes: ~3–5 years with unpaid rent/no contact

(Exact timelines vary by state and property category.)

Myths vs. facts

Myth: “Unclaimed means the state took my money.”

Fact: Programs act as custodians. Owners/heirs generally retain perpetual rights to claim.

Myth: “If I didn’t get a notice, I don’t have anything.”

Fact: Bad addresses and spam filters are the whole problem. You may still have a match.

Myth: “It only happens to people who are disorganized.”

Fact: It happens to organized people too—life events and system errors don’t discriminate.

Simple habits that keep money from “disappearing”

- Update contact details everywhere after a move or name change (banks, payroll, insurers, brokerages, utilities, card issuers, retirement plans).

- Consolidate or close dormant and duplicate accounts to reduce stragglers.

- Turn on alerts (email/SMS) and scan statements quarterly—especially around job changes or relocations.

- Keep a one-page inventory of accounts, policies, and safe-deposit boxes; note login emails and prior addresses tied to each.

- Open the “boring” mail. Refunds and dividends often arrive in plain envelopes.

- For families and estates: Document beneficiaries, store policy/plan details, and designate a trusted person who knows where records live.

What to do right now (quick game plan)

- Search your full name plus prior names (e.g., maiden, hyphenated) and former addresses/cities.

- Check for family you manage paperwork for—spouses, parents, estates, and small businesses.

- Gather basics you’ll likely need to claim: government ID and proof of current address; for estates, death certificate and authority documents.

- Set a cadence: Add a calendar reminder to re-check once or twice a year, especially after moves, job changes, or major life events.

Unclaimed money is usually a paperwork problem, not a personal failing. Our financial lives rely on tidy records and perfect contact data; real life rarely cooperates. Small oversights and routine errors compound over time, and balances drift to “unclaimed.” A periodic search plus cleaner contact info keeps your money connected to you—and gets it back when it slips.