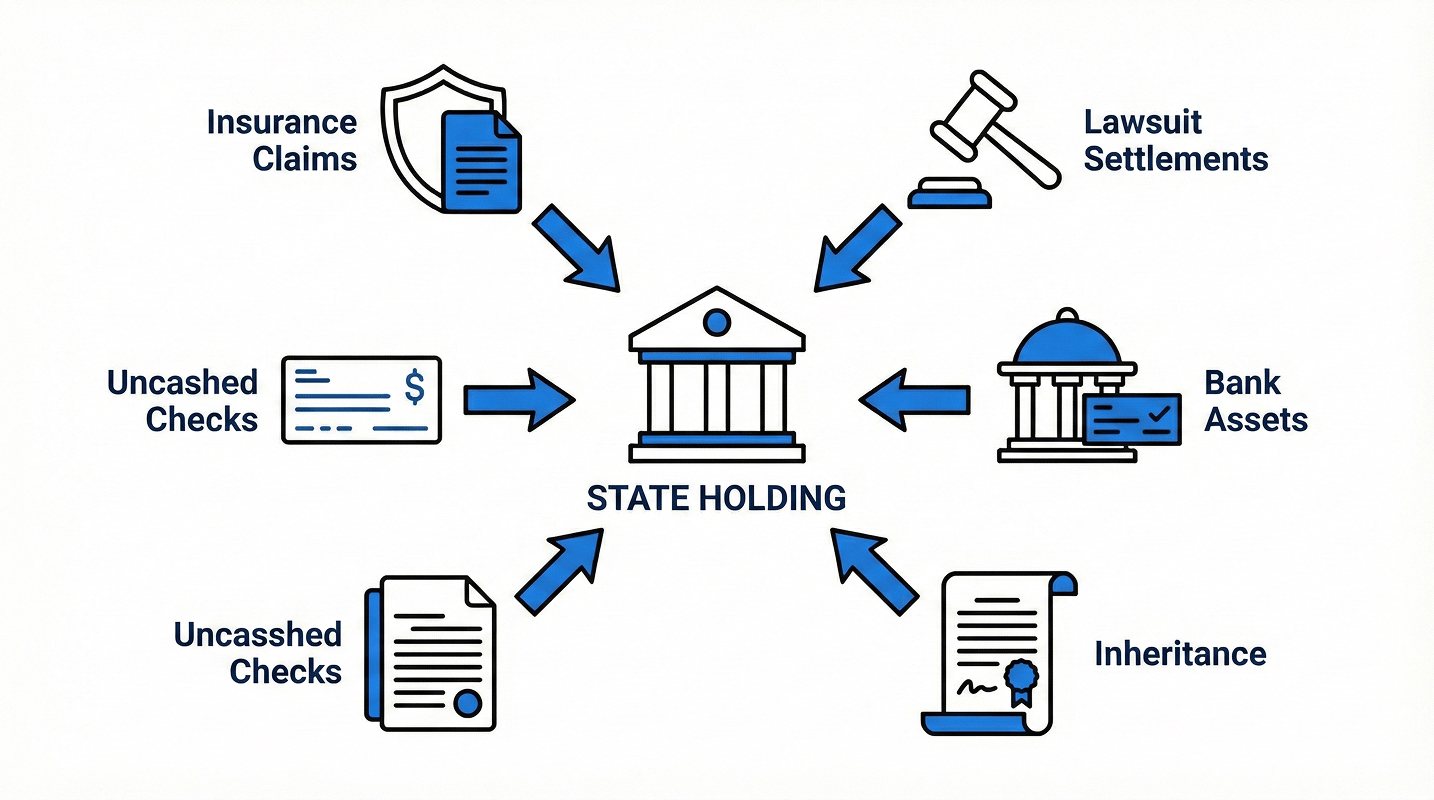

What Are “Unclaimed Assets”?

Unclaimed assets (also called unclaimed property or abandoned property) are financial assets that have lost contact with their owners for a legally defined period. After that dormancy window, the assets are transferred to state custody through escheatment. The state acts as custodian—not owner—until the rightful owner or heirs are located and the funds are returned.

These laws exist for consumer protection: rather than letting companies hold forgotten balances indefinitely, states maintain records, safeguard value, and work to reunite property with its owners.

Types of Unclaimed Assets

Financial assets

- Dormant bank accounts (checking, savings, CDs)

- Uncashed checks and money orders

- Insurance benefits and annuity payments

- Unclaimed wages and pension benefits

- Stocks and dividends, bond interest, and brokerage accounts

- Utility deposits and refunds

Tangible property

- Contents from abandoned safe deposit boxes

- Jewelry and precious metals

- Collectibles and artwork

- Personal items with historical or sentimental value

Business-related assets

- Unclaimed vendor payments

- Customer deposits and credits

- Uncashed payroll checks

- Business insurance proceeds

How Escheatment Works (Overview)

Most states follow versions of the Uniform Unclaimed Property Act (UUPA) with local variations. The flow is generally:

1) Dormancy period

Each property type has a period of inactivity before it’s presumed unclaimed. Typical windows:

- Bank accounts: 3–5 years of no activity

- Insurance proceeds: 3–7 years after due and payable

- Wages: 1–3 years after payable date

- Safe deposit boxes: 3–5 years of no contact

2) Due diligence by the holder

Before reporting to the state, companies make good-faith efforts to find the owner, such as:

- Sending written notice to the last known address

- Searching internal systems for updated contact info

- (In some cases) using professional locator services

- Publishing legal notices for certain high-value items

3) Reporting & remittance

Holders file an annual report with the state (treasurer/comptroller/DFS), including:

- Property descriptions and values

- Owner information (as available)

- Contact attempts and holding history

- Confirmation of due-diligence steps

After reporting, the holder remits the asset (or cash equivalent) to the state.

How States Administer Unclaimed Property

Safekeeping

States preserve the value of liquid assets and provide appropriate storage and care for tangible items. For cash, many programs maintain interest-bearing or pooled accounts; for physical items, states manage secure storage until disposition rules apply.

Records & transparency

States keep comprehensive records that typically include:

- Property descriptions and estimated value

- Owner identifiers (as reported)

- Source of property and date received

- Claim history and status updates

Public access

Most programs offer free, searchable databases so people can look up property under their name(s). These sites are regularly updated.

Outreach

States use proactive outreach—media campaigns, direct mail, community events, and partnerships (including genealogical/heir-search efforts)—to increase reunions.

How to Claim Your Property

Initial claim

You’ll complete a claim form with:

- Personal information

- Proof of identity (e.g., driver’s license, passport)

- Proof of entitlement to the asset (varies by type)

- Documentation connecting you to the property (as required by the state)

Documentation (varies by case)

Common requests include:

- SSN or ITIN (for verification/tax reporting, where applicable)

- Proof of current or historical address (utility bill, lease, statement)

- For deceased owners: death certificate, probate/letters of administration

- For businesses: formation documents, EIN confirmation, authorized-signer ID

Review & processing

The state verifies identity and entitlement, cross-checks with holder records, and may request additional information for complex situations (multiple owners, estates/trusts).

Payment & recovery

After approval, payment is typically issued within 30–90 days via:

- State-issued check or direct deposit (as available)

- For tangible items: scheduled pickup or shipping per program rules

Legal Framework & Compliance

Constitutional due process

States must provide adequate notice and opportunity to claim before final disposition, consistent with the Fourteenth Amendment.

Interstate priority rules

When owners and holders are in different states, priority rules determine which state has custody, preventing double claims and promoting consistency.

Audits & enforcement

States audit holders to ensure compliance. Potential outcomes:

- Assessment of previously unreported property

- Interest/penalties for non-compliance

- Compliance training or enhanced reporting for repeat issues

Scale & Economic Impact

National picture

- Roughly tens of billions of dollars are held by states at any given time.

- States collectively return billions annually to owners.

- Average claims often fall in the hundreds to low thousands, though some exceed $100,000.

Program variation

- Large states (e.g., California, New York) hold multi-billion-dollar inventories.

- Smaller states may hold hundreds of millions.

- Annual return rates typically represent a fraction of total holdings, as new property continuously flows in while claims are paid out.

Myths vs. Facts

“The state keeps my money.”

False. States act as custodians. Owners and heirs generally retain perpetual rights to claim.

“I have to pay to search or file.”

False. Official state searches and claims are free. Be cautious of third parties charging fees for services the state provides at no cost.

“Any email/letter about unclaimed money is legit.”

Not necessarily. Use official state portals or verified notices. Avoid sharing sensitive information via unsolicited calls or emails.

Practical Tips to Avoid Escheatment

Individuals

- Keep addresses and email/phone current with financial institutions.

- Review statements and follow up on missing mail.

- Maintain a consolidated list of accounts, policies, and safe deposit boxes.

- Let a trusted contact know where records are kept.

- Consider a durable power of attorney for emergencies.

Businesses

- Maintain clean customer/vendor master data and change-of-address procedures.

- Track returned mail and uncashed checks.

- Create standard operating procedures for due diligence and reporting.

- Conduct periodic internal reviews to identify potential unclaimed items.

- Consider specialized compliance support if volume/complexity is high.

What’s Changing: Trends to Watch

Digital assets

States are clarifying rules for cryptocurrency and digital wallets, including how to determine dormancy, value, liquidation, and owner verification.

Better tech

Agencies are upgrading databases, matching tools, portals, and e-filing, improving accuracy and accelerating returns.

Interstate coordination

Enhanced adoption of uniform standards and data formats aims to reduce friction in multi-state property scenarios.

Conclusion

Unclaimed-property programs are a core consumer-protection function that return billions of dollars each year. Knowing how escheatment works—and checking periodically—helps keep your money in your hands. The combination of public awareness, better technology, and clearer statutes continues to improve outcomes for owners and heirs.

For nationwide links to state programs, the National Association of Unclaimed Property Administrators (NAUPA) provides a directory of official sites. Regular searches—paired with good record-keeping—are the simplest way to prevent assets from drifting into state custody in the first place.